If you've ever wondered how a modest, regular investment turns into a life-changing corpus, the answer isn't a hot stock tip or perfect market timing. It's compounding — quietly, patiently, doing the heavy lifting in the background while you go about your life. At A2 Wealth, we believe this is the single most underrated force in personal finance, and once you actually see the numbers, it changes how you think about every rupee you invest.

What Is the Power of Compounding?

Compounding is the process by which your investment returns start earning their own returns. Instead of earning a flat amount each year, your gains get added back to your principal, so the next year's growth is calculated on a larger base. The result isn't a straight line — it's a curve that bends upward, slowly at first, then dramatically.

This is different from simple interest, where you only ever earn on your original investment. Over short periods, the difference looks small. Over decades, it becomes the difference between a comfortable retirement and a stretched one — a point HSBC India's primer on compounding also makes well: compounding isn't a get-rich-quick scheme, it's a patient strategy for gradual wealth creation.

A line often (though not verifiably) attributed to Einstein captures it well: compound interest is sometimes called the "eighth wonder of the world" — because those who understand it benefit from it, and those who don't end up paying for it through inflation, debt, or lost opportunity.

Key takeaway: Compounding rewards time more than it rewards timing. The earlier you start and the longer you stay invested, the less effort you need to put in for the same outcome.

Simple Interest vs. Compound Interest: Why the Gap Widens

Here's the core distinction, stripped of jargon:

| Feature | Simple Interest | Compound Interest |

|---|---|---|

| Calculated on | Original principal only | Principal + accumulated returns |

| Growth pattern | Linear (straight line) | Exponential (curved, accelerating) |

| Best suited for | Short-term, fixed-return instruments | Long-term wealth creation |

| Typical use | Some loans, basic FDs | Equity mutual funds, reinvested SIPs |

On ₹1 crore invested for 20 years at 10%, simple interest gets you to ₹3 crore. Compound interest at the same 10% gets you to ₹6.7 crore — more than double, for the exact same rate of return. The only difference is whether your gains are allowed to keep working.

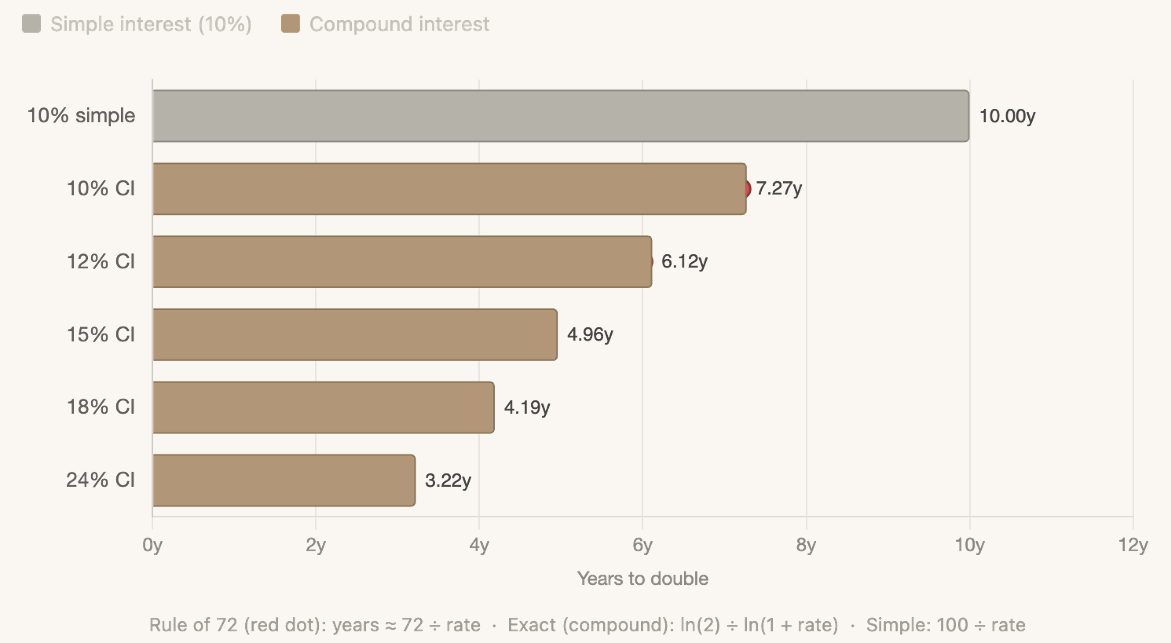

The Rule of 72: A Quick Way to See Time at Work

A handy mental shortcut for estimating how long money takes to double is the Rule of 72 — a method Fiducient Advisors describes as a quick way to forecast compound growth without reaching for a calculator: divide 72 by your expected annual return.

- At 12% compound growth, 72 ÷ 12 = 6 years to double

- At 18% compound growth, 72 ÷ 18 = 4 years to double

- At 24% compound growth, 72 ÷ 24 = 3 years to double

The table below shows this in full, comparing simple interest to compound interest at various rates:

| Rate of Return | Time to Double |

|---|---|

| 10% Simple Interest | 10.00 years |

| 10% Compound Interest | 7.27 years |

| 12% Compound Interest | 6.12 years |

| 15% Compound Interest | 4.96 years |

| 18% Compound Interest | 4.19 years |

| 24% Compound Interest | 3.22 years |

Notice something important: the gap between simple and compound interest at the same 10% rate is already nearly 3 years. As the rate of return rises — which is realistic for equity-oriented mutual funds — the doubling time shrinks fast, and that's where compounding starts to feel less like math and more like magic.

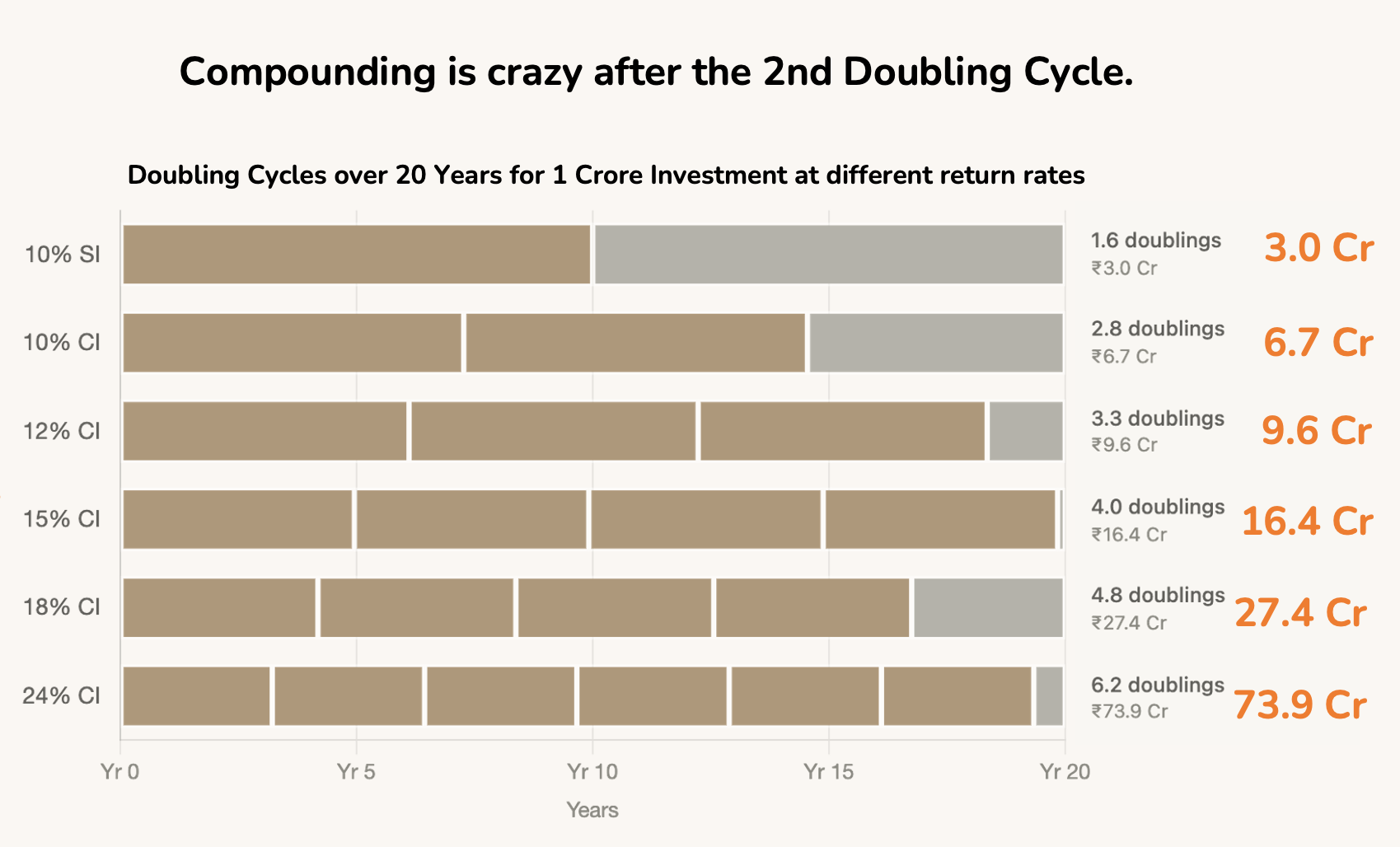

Why Compounding Gets "Crazy" After the Second Doubling Cycle

This is the part most investors underestimate. Each time your money doubles, the next doubling adds a far bigger absolute amount — because it's doubling a bigger number.

Consider ₹1 crore invested for 20 years at different rates:

| Strategy | Doublings in 20 Years | Final Corpus |

|---|---|---|

| 10% Simple Interest | 1.6 | ₹3.0 Cr |

| 10% Compound Interest | 2.8 | ₹6.7 Cr |

| 12% Compound Interest | 3.3 | ₹9.6 Cr |

| 15% Compound Interest | 4.0 | ₹16.4 Cr |

| 18% Compound Interest | 4.8 | ₹27.4 Cr |

| 24% Compound Interest | 6.2 | ₹73.9 Cr |

Look closely at the jump from 12% to 24%. The rate only doubled, but the final corpus grew more than 7.5 times over. That's not a rounding effect — it's the nature of exponential growth. Once you're past the first two or three doubling cycles, every additional year of staying invested does more work than all the years before it combined.

This is precisely why financial advisors are almost obsessive about two things: starting early, and not interrupting the compounding chain by withdrawing midway.

One honest caveat worth flagging: real markets don't compound in a smooth, straight line the way these illustrative tables do. As Zerodha Varsity explains in its piece on why the compounding effect isn't linear, actual returns move in a volatile curve — full of sharp dips and sudden rallies — that only averages out to a steady CAGR over long periods. This is exactly why staying invested through the bumpy years matters as much as the rate of return itself.

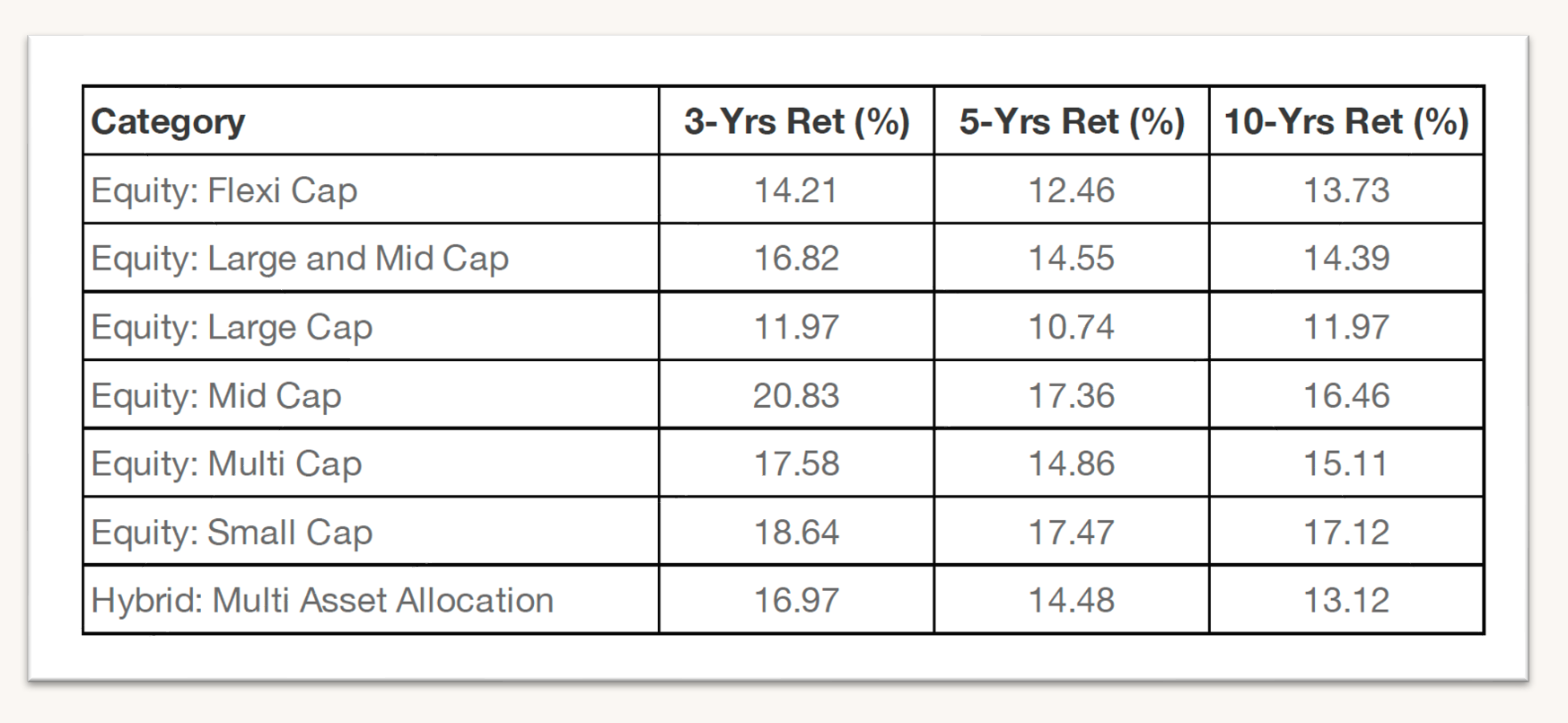

How Much Have Mutual Funds Actually Returned Over the Long Term?

The numbers above use illustrative compounding rates. The natural next question is: what returns do real mutual funds actually deliver? Here's category-wise data showing average annualised returns over 3, 5, and 10 years:

| Category | 3-Yr Return (%) | 5-Yr Return (%) | 10-Yr Return (%) |

|---|---|---|---|

| Equity: Large Cap | 11.97 | 10.74 | 11.97 |

| Equity: Flexi Cap | 14.21 | 12.46 | 13.73 |

| Equity: Large & Mid Cap | 16.82 | 14.55 | 14.39 |

| Equity: Multi Cap | 17.58 | 14.86 | 15.11 |

| Equity: Mid Cap | 20.83 | 17.36 | 16.46 |

| Equity: Small Cap | 18.64 | 17.47 | 17.12 |

| Hybrid: Multi Asset Allocation | 16.97 | 14.48 | 13.12 |

In other words, depending on the category and the risk you're comfortable taking, long-term equity mutual fund returns have broadly ranged from around 12% in more conservative large-cap funds to over 17–20% in mid-cap and small-cap funds, with hybrid, multi-asset categories sitting somewhere in between for investors who want a smoother ride. These are category averages, not guarantees — actual fund performance varies, and past returns never assure future ones.

This range is consistent with independently tracked industry data. Equentis' analysis of AMFI figures shows the average return on SIP investments in India over the last 10 years has ranged between roughly 11% and 14% for equity mutual funds, with equity SIPs held for 20 years in diversified and flexi-cap funds historically delivering 13–16% annually. Separately, FinEdge's review of 10-year SIP performance shows average SIP returns measured by XIRR have consistently fallen in the 12–15% range for equity funds.

Now map this back to the compounding table above: even the "conservative" end of equity mutual fund returns (12%) sits in the same zone as the 12% CI row that turned ₹1 crore into ₹9.6 crore over 20 years. Push into mid-cap or small-cap territory, and you're closer to the 18% row — nearly ₹27.4 crore on the same ₹1 crore base. This is exactly why "average" returns, sustained over long horizons, can look extraordinary in hindsight even though nothing about the underlying rate was unusual in any single year.

Why Mutual Funds Are Particularly Suited to Compounding

Mutual funds don't pay a fixed "interest rate" the way a fixed deposit does. Instead, their Net Asset Value (NAV) reflects the underlying value of stocks, bonds, or other assets the fund holds, and that value is recalculated daily. When you choose the growth option, every gain the fund makes is automatically retained and reinvested rather than paid out — which means your future returns are calculated on an ever-growing base, exactly the mechanism compounding depends on.

Systematic Investment Plans (SIPs) take this a step further by adding discipline to the equation. Every monthly instalment starts compounding from its own investment date, so a SIP that runs for 15–20 years effectively has thousands of "mini compounding clocks" running simultaneously — early instalments doing the most work, later ones still contributing. This is also why staying invested through volatility matters more than trying to time entries and exits: Outlook India's analysis of the latest AMFI data found SIPs started during market lows tend to generate comparatively higher returns when held for long periods, reinforcing the case for continuous, disciplined investing rather than reactive stop-start behaviour.

How to Make Compounding Work for You: 5 Practical Rules

Start as early as you can. Time, not the size of your first investment, is the most powerful variable in the compounding formula. A smaller amount invested for 25 years will often outgrow a larger amount invested for 15.

Stay invested — don't break the chain. Every withdrawal resets part of your compounding base. Even necessary withdrawals should be planned around your goals, not market noise.

Increase your SIP as your income grows. Stepping up your SIP by even 10% a year keeps your contributions compounding alongside your career growth, not lagging behind it.

Keep an eye on costs. Fees quietly erode compounding over decades. Fiducient Advisors illustrates this with a simple example: on a $1 million portfolio growing at 8% annually, a 0.1% annual fee versus a 0.5% fee creates a gap of over $1 million after 30 years — the cost isn't just the fee itself, but the compounding you lose on that fee.

Don't wait for the "right" time to start. Delay is the most expensive mistake in compounding. The same Fiducient analysis shows a $10,000 investment earning 7% annually grows to roughly $76,000 in 30 years, but waiting just five years to begin reduces that to around $54,000 — a gap created purely by procrastination, not by market performance.

Common Mistakes That Break the Compounding Chain

- Chasing last year's best-performing fund instead of staying with a suitable, well-structured portfolio.

- Pausing SIPs during market corrections — historically one of the costliest behavioural mistakes, since corrections are often when long-term compounding gets its best entry points.

- Treating long-term investments like a savings account and withdrawing for non-essential expenses.

- Ignoring asset allocation and taking either too much or too little risk relative to your goal's time horizon.

- Not reviewing the plan periodically — compounding works best within a structure, not on autopilot with no oversight.

Key Takeaways

- Compounding means your returns earn returns — growth accelerates rather than staying flat.

- The Rule of 72 (72 ÷ rate of return) gives a quick estimate of how long your money takes to double.

- The real wealth-building happens after the second or third doubling cycle — patience compounds too.

- Equity mutual fund categories have historically delivered roughly 12% to 20%+ CAGR over the long term, depending on the risk taken; these are historical averages, not assured returns.

- SIPs combine disciplined investing with the natural compounding mechanism of growth-option mutual funds.

- Time in the market, low costs, and staying invested matter more than trying to time entries and exits.

Further Reading & Sources

This article draws on data from A2 Wealth's internal analysis alongside the following external resources, if you'd like to go deeper:

- HSBC India — How the Power of Compounding Builds Wealth Over Time

- Fiducient Advisors — The Power of Compounding: How Time Can Be Your Best Investment Ally

- Zerodha Varsity — The Compounding Effect Is Not Linear

- Outlook India — SIP Returns in Equity Mutual Funds: What Latest AMFI Data Shows

- FinEdge — What Is the Real SIP Return After 10 Years?

- Equentis — Average Return on SIP: What to Expect & How to Maximize Investment

Watch

A short, plain-language explainer on the power of compounding in everyday investing.

Frequently Asked Questions

What is the power of compounding in simple words?

It's the effect of earning returns not just on your original investment, but also on the returns that investment has already generated — so your money grows at an accelerating, rather than constant, rate.

How does the Rule of 72 work?

Divide 72 by your expected annual rate of return to estimate how many years it will take for your investment to double. For example, at 12% annual returns, 72 ÷ 12 = 6 years.

What is the 8-4-3 rule of compounding?

It's a popular way of visualising compounding in three phases — roughly 8 years of steady, modest-looking growth, the next 4 years where growth visibly accelerates, and a final phase where the bulk of the wealth appears to build almost overnight. The exact years vary with the assumed rate of return, but the principle — that growth backloads itself — holds across rates.

Do mutual funds compound automatically?

Yes, when you choose the growth option. Gains are reinvested into the fund rather than paid out, so your future returns are calculated on a continuously growing NAV-based value.

What returns can I realistically expect from equity mutual funds over the long term?

Based on long-term category averages, large-cap funds have historically delivered around 12% CAGR, while mid-cap and small-cap categories have averaged closer to 17–20%+ CAGR over 10-year periods. Actual returns vary by fund, market cycle, and time horizon, and past performance is not a guarantee of future results.

Is a SIP better than a lump sum for compounding?

Both compound once invested. SIPs add the benefit of rupee-cost averaging and behavioural discipline, making them easier to sustain over long periods — which is often what determines whether compounding actually gets the time it needs to work.

How long should I stay invested to really see compounding work?

Most of the visible "magic" happens after 10–15 years, once you're past the first two or three doubling cycles. This is why goal-based, long-horizon investing consistently outperforms short-term, reactive investing.

The Bottom Line

Compounding isn't a strategy you execute once — it's an environment you protect over years and decades. The mathematics is identical whether you're an HNI structuring a multi-goal portfolio or a salaried professional starting your first SIP: more time and fewer interruptions beat a slightly higher return chased through frequent switching. Wealth is built in years, not days, and every rupee you invest today is simply buying itself more time to grow.

Want to talk?

If you'd like help structuring a long-term, goal-based investment plan that lets compounding do its job — want to talk? Get in touch with A2 Wealth today.