Meet Arjun.

He's 34, works at a good company in Bengaluru, takes home ₹1.2 lakh a month, and has done so for the last five years. His LinkedIn looks great. He got two promotions. His family is proud.

But last month, when his car needed an ₹80,000 repair, he had no savings to fall back on. He ended up converting it into a smartEMI on his credit card at the end of the month, because there was simply nothing else left.

Five years of earning ₹1.2 lakh a month (that's over ₹70 lakhs of gross income) and an ₹80,000 emergency sent him straight to his credit card.

Arjun isn't careless. He isn't reckless. He just never understood why his salary kept disappearing. Sound familiar?

This is the most common financial story in urban India right now. And it has nothing to do with how much you earn. It has everything to do with how your money flows.

The Leaky Bucket: Why Your Salary Disappears Every Month

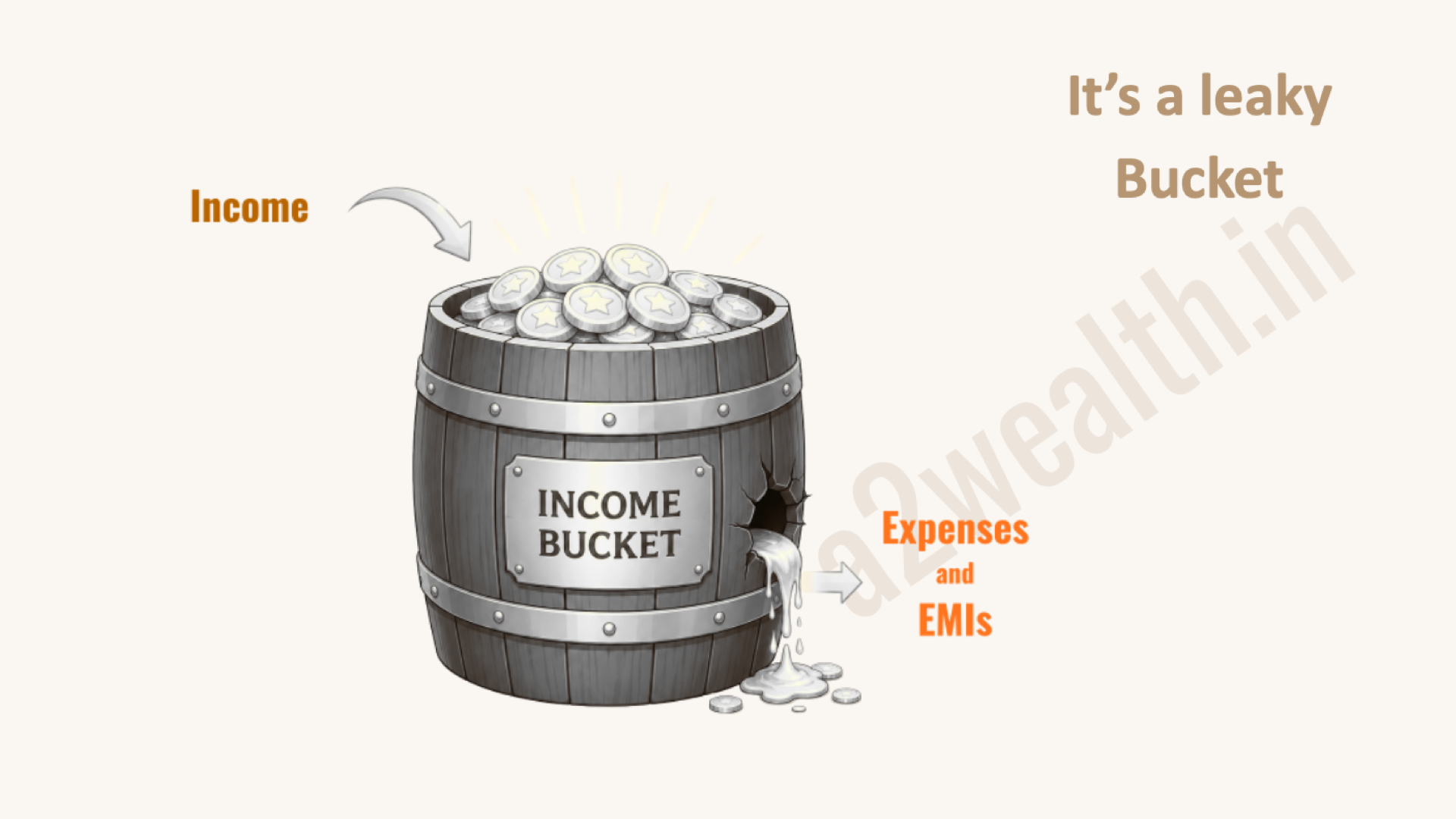

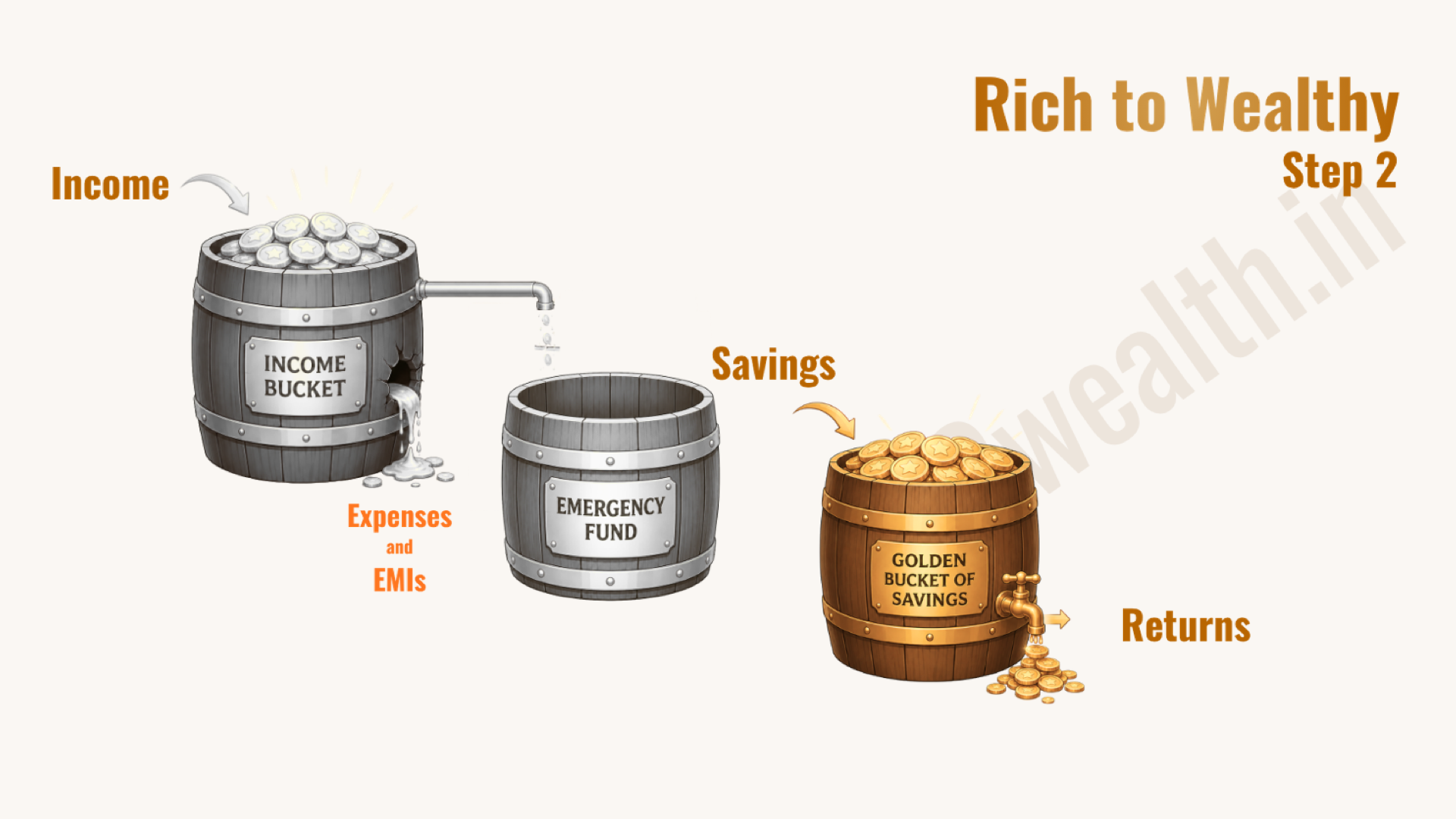

Think of your income as water being poured into a bucket.

Every month, your salary fills it up: steady, reliable, reassuring. But there's a hole in the side. A big one. And through that hole flows everything: rent, EMIs, groceries, subscriptions, the occasional impulsive online order, the weekend dinners that add up faster than you think.

By the end of the month, the bucket is nearly empty. You pour in more next month. It empties again. The cycle repeats for years.

This is the financial reality for a huge number of salaried Indians. India's household savings rate dropped to just 18.1% of GDP in FY2024 (the third consecutive year of decline) even as incomes in urban India have grown steadily. Annual household borrowings have climbed to 5.8% of GDP, the highest level since the 1970s. We are, as a country, collectively spending more, saving less, and borrowing more, even as salaries rise.

The bucket has a hole. And most of us are just pouring more water in, hoping it'll stay full.

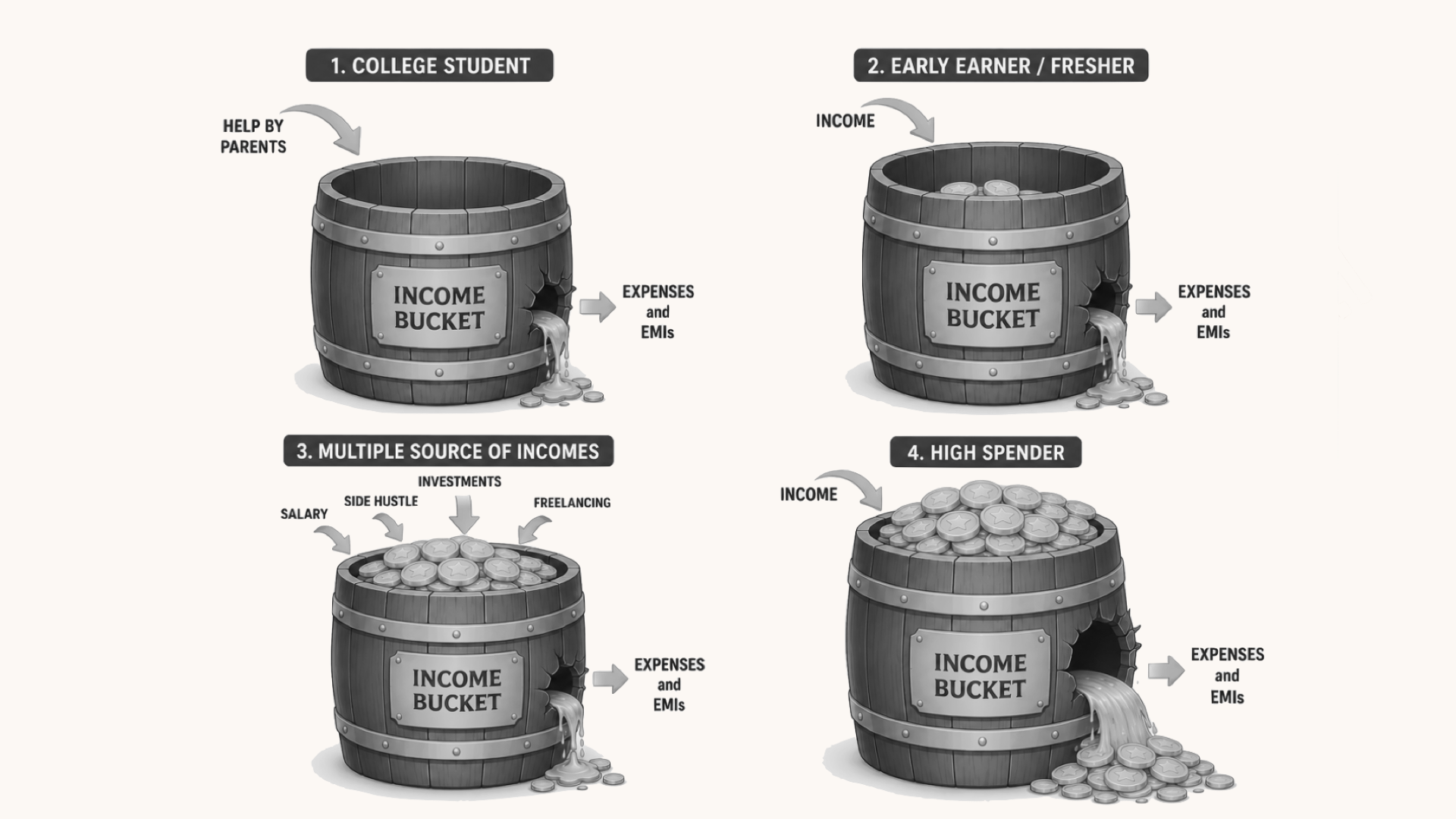

What does that leak look like in real life? It's not always big, dramatic splurges. It's subtler than that.

- The college student whose parents fill the bucket; expenses drain it.

- The early earner with a first salary, expenses, and an EMI or two.

- The person with multiple income sources (salary, side hustle, freelancing) but whose lifestyle has expanded to consume all of it.

- And then there's the high spender: the one earning the most, but with the biggest hole.

That last one is where it gets interesting, and uncomfortable.

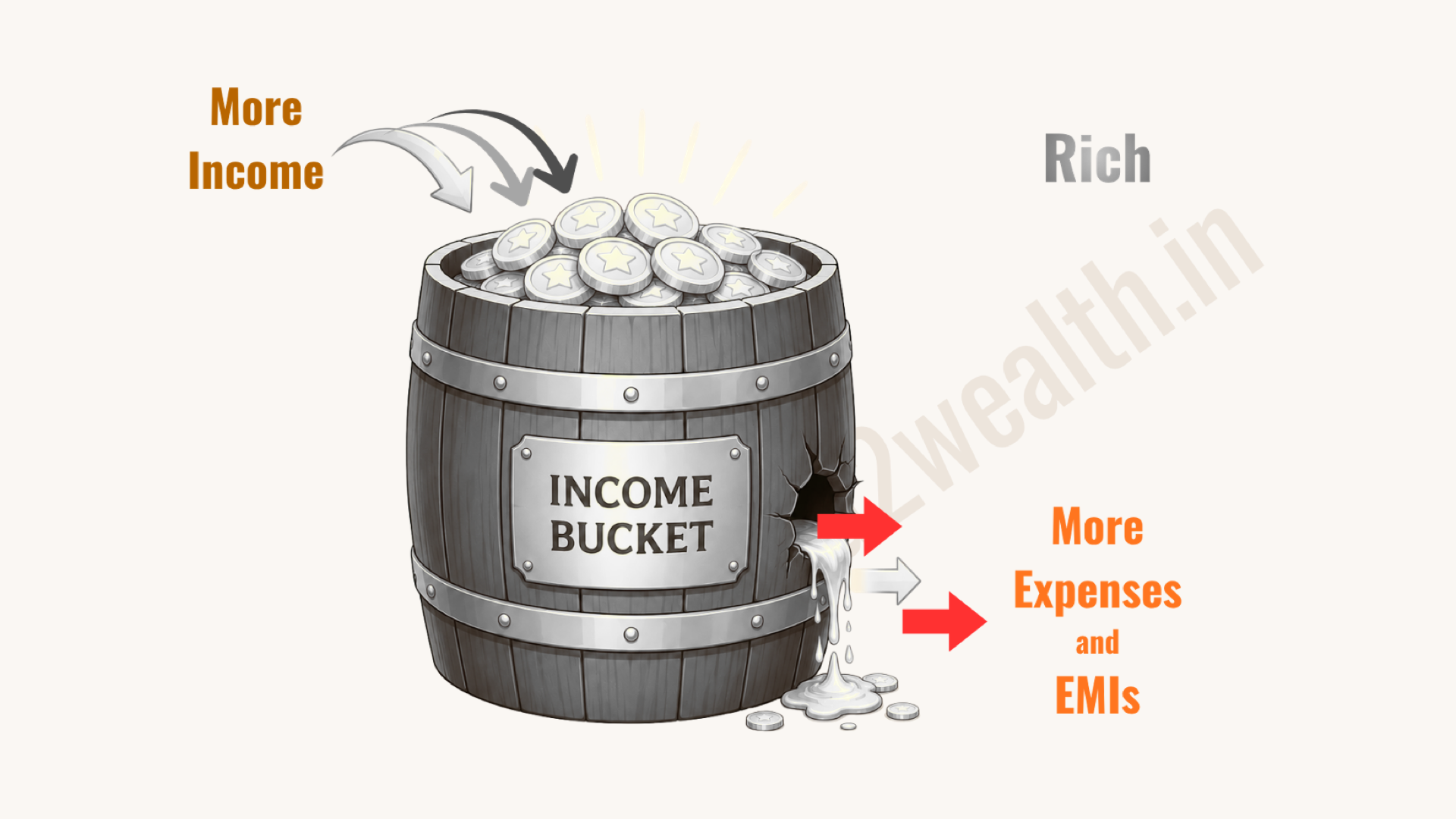

The "Rich" Trap: Why a Raise Won't Fix the Problem

Here's what most people believe: if I just earned more, I'd be fine.

So they chase the promotion. They negotiate harder at appraisals. They take on more work. And when the raise comes (and it does come), something strange happens.

The new car feels justified. The bigger apartment makes sense now. The nicer restaurants don't feel like an indulgence anymore. The lifestyle expands to meet the new income. And within a few months, the end-of-month feeling is exactly the same as before.

This is what economists call lifestyle inflation, and it's relentless. Research tracking urban Indian professionals found that a ₹20 lakh per year earner who saves 30% and invests consistently will, over time, significantly outpace a ₹35 lakh earner who lifestyle-inflates their spending to 90% of income and relies only on EPF. The higher earner feels richer. They are not building more wealth.

The bucket got bigger. But so did the hole.

"Higher income alone doesn't make you wealthy. It just means a bigger bucket with a bigger hole. Wealth starts with a different habit."

This is the core insight that separates people who earn well from people who build wealth. It's not about the amount flowing in. It's about what you do before it flows out.

Ankur Warikoo, one of India's most trusted voices on personal finance, describes it similarly in his widely watched video on the three paths of money: the poverty mindset spends everything, the middle-class mindset converts income into liabilities that look like wealth (the car, the flat on EMI), and the wealth mindset converts income into assets that generate more income. The bucket framework is, at its heart, the same idea, made visible.

The Journey from Salaried to Wealthy: Three Steps

So what does the shift actually look like? It's not a single dramatic decision. It's a sequence: three deliberate steps that change how money moves through your life.

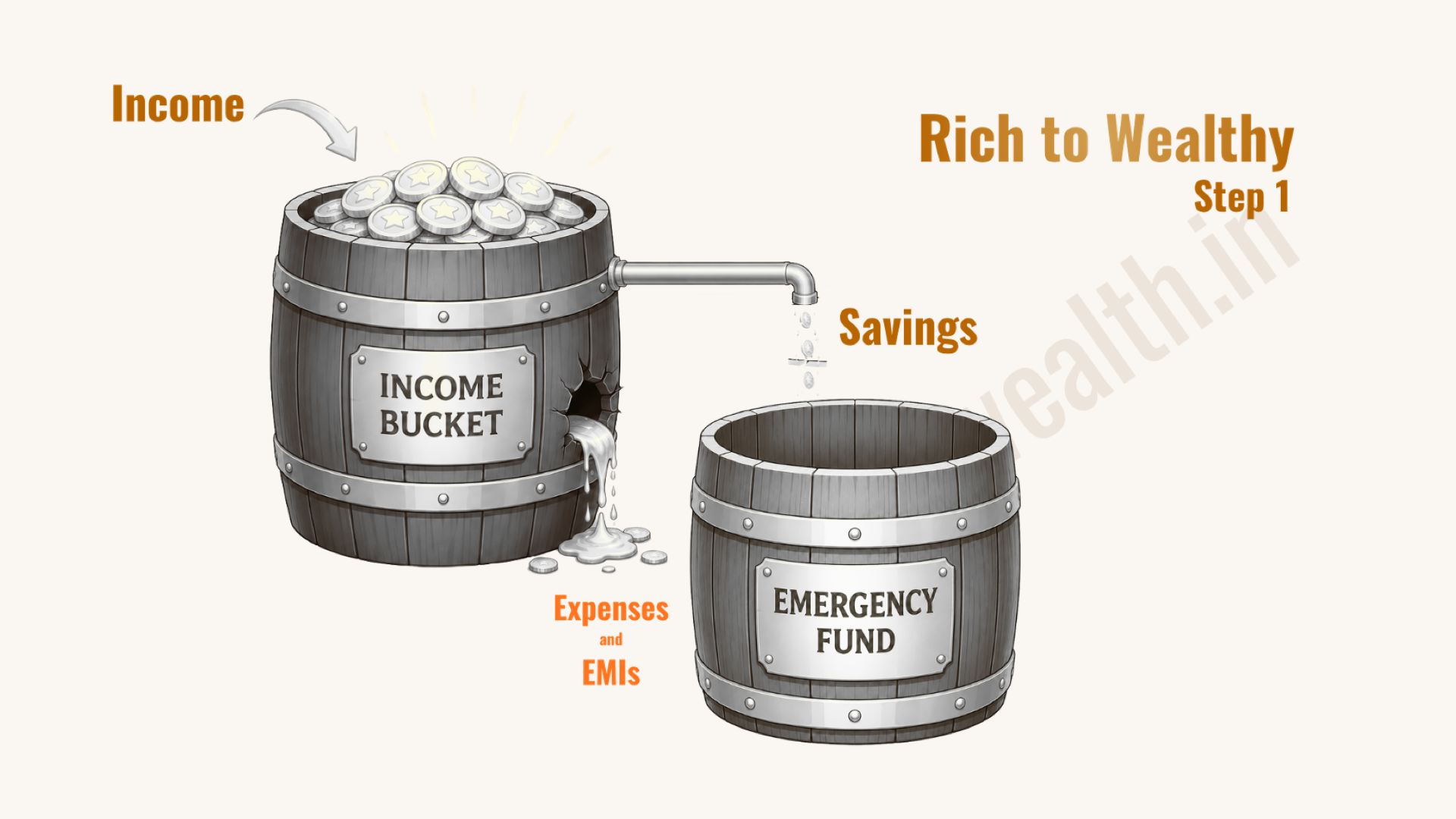

Step 1 - Plug the Leak (Build Your Emergency Fund)

The first move is deceptively simple: before your money hits your expenses, redirect a fixed portion of it somewhere safe.

Not invested. Not locked away. Just separate: a dedicated emergency fund that you don't touch unless life actually breaks down.

This is the pipe that gets added to the income bucket. Instead of everything draining through the hole, a small stream is deliberately diverted, quietly and automatically, into an emergency fund sitting beside your main account.

Why start here? Because without this buffer, every financial emergency becomes a crisis. The car repair. The medical bill. The job loss. Without a safety net, any of these sends you to your credit card or a personal loan, setting you back months or years. The emergency fund is not where wealth is built. It's what makes wealth-building possible.

A standard target: 3 to 6 months of your total monthly expenses, parked in a liquid instrument (a liquid mutual fund or a high-interest savings account) that you can access within 24-48 hours if you need it.

Set up an automatic transfer on salary day. Treat it like an EMI you owe yourself.

Step 2 - Create the Golden Bucket (Start Investing)

Once your emergency fund is in place (or even while you're building it), the next step is to redirect surplus into a separate investment bucket. This is where the real shift begins.

In the visual, this bucket is golden, and deliberately so. This isn't just savings sitting in a bank account earning 3%. This is money put to work: in equity mutual funds through a monthly SIP (Systematic Investment Plan, a fixed amount auto-invested every month, much like an EMI, but one that builds your wealth instead of someone else's), in index funds, in debt funds for your medium-term goals.

The golden bucket doesn't just hold money. It generates returns. Those returns add to the bucket. The bucket grows. And critically, this bucket also has a tap. That tap drips returns back out into your life.

Consider a straightforward example: a salaried professional who invests ₹50,000 per month in equity mutual funds averaging 12% annual returns (which is consistent with Nifty 50's historical long-term CAGR) over 25-30 years builds a corpus sufficient for complete financial independence. The math works because of compounding. And compounding only works if you stay invested long enough for it to matter.

The biggest mistake people make at this stage is waiting. Waiting until the salary is higher. Waiting until the EMI is paid off. Waiting until things settle down. Things never settle down. The best time to start the golden bucket is now, with whatever you can redirect, even ₹5,000 a month.

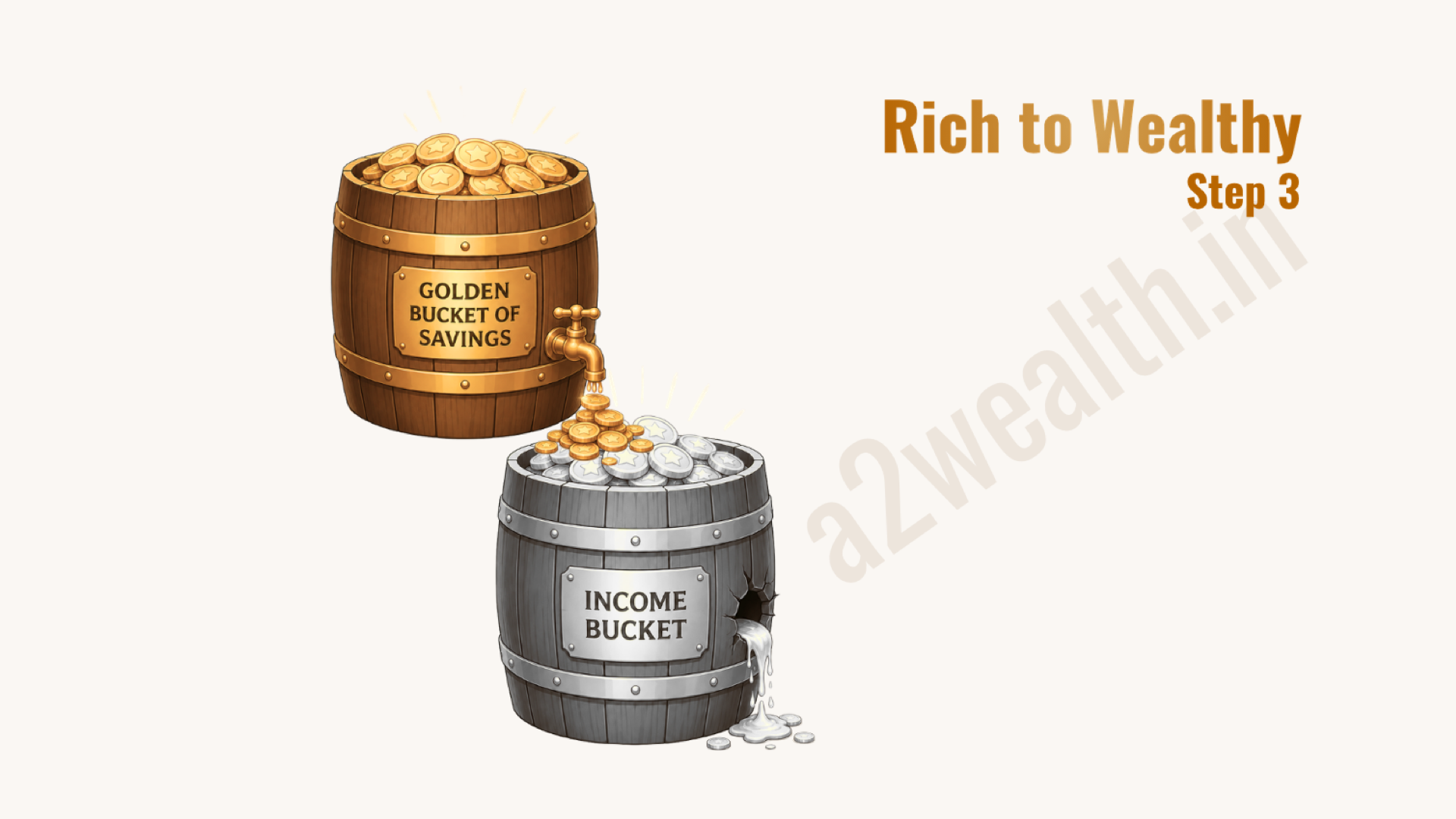

Step 3 - The Cascade (Let Your Wealth Work for You)

This is the step that most people never reach, not because it's hard, but because they never took steps 1 and 2 seriously enough.

When your golden bucket grows large enough, its returns start to overflow into another bucket. That bucket generates its own returns, which overflow into another. Multiple golden buckets, feeding each other: a cascade of compounding wealth.

This is what compounding looks like when you visualise it properly. Not a graph. Not a number. A waterfall, each bucket filling the next, the whole system becoming self-sustaining over time.

At this stage, your investments are generating income that doesn't depend on your monthly salary. Your wealth is no longer just a function of how much you earn at work. It has its own momentum.

This is the difference between being rich (a bigger income bucket) and being wealthy (a cascade of golden buckets). The wealthy person can lose their job and still be fine. The rich person cannot.

Why Most People Never Make This Shift

Here's the thing: the bucket framework isn't complicated. Most people reading this already understand the logic. So why don't more people actually do it?

The honest answer: it's not a financial problem. It's a behavioural one, and it runs deeper than just "lack of discipline."

Spending feels immediate. Investing feels abstract. The new phone is real. The retirement corpus is theoretical. Our brains are wired to favour today's pleasure over tomorrow's security, what psychologists call present bias. This is why the "I'll start investing next month" intention almost never becomes action.

Lifestyle inflation is invisible while it's happening. Nobody consciously decides to upgrade their lifestyle every time they get a raise. It just happens: a slightly better restaurant here, a subscription added there, a car upgrade that seems perfectly reasonable given the new salary. By the time you notice, the new lifestyle feels like a necessity, not a choice.

Social comparison keeps the hole open. In India's urban professional circles, what you drive, where you holiday, and which school your child attends carry enormous social weight. Keeping pace with peers is an invisible but powerful force that keeps spending high and savings low. As one financial commentator puts it, the trap is "socially reinforced": friends who also got hikes are upgrading, and Instagram shows a curated feed of aspirational living.

The absence of a plan means money has no destination. When there's no SIP set up, no emergency fund target, no investment goal tied to a real life milestone (retirement, children's education, a home), money simply flows wherever it's pulled. And it's always pulled toward the present.

But there's a fifth reason, and it may be the most important one.

Most people genuinely cannot picture how their golden bucket will ever replace their salary. And because they can't see it, they don't believe it. And because they don't believe it, they never truly commit to it.

Think about it from the inside: you're earning ₹80,000 a month. You set aside ₹8,000 in a SIP. Twelve months later, you have roughly ₹1 lakh invested, which generates maybe ₹10,000-12,000 a year in returns. That's less than ₹1,000 a month. It feels completely pointless. It feels like it will take 200 years to matter.

So you stop. Or you never start meaningfully.

What's missing is an understanding of how compounding actually works, not in theory, but numerically, over time. The returns in year 1 feel laughably small. But they are not small. They are the foundation. Because in year 10, that same consistent ₹8,000 per month SIP, at 12% annual returns, has already grown to roughly ₹18 lakh, generating over ₹2 lakh a year in returns, or nearly ₹18,000 a month. In year 20, the corpus crosses ₹80 lakh. And the returns from that corpus alone start to meaningfully supplement, and eventually rival, your monthly salary.

The problem isn't discipline alone. The problem is that people try to stay disciplined toward a goal they can't visualise, and so the motivation collapses long before the compounding has had time to build momentum.

This is exactly why we wrote a dedicated piece on the power of compounding, because once you actually see the numbers play out over 15-20 years, the motivation to stay invested stops being an act of willpower. It becomes obvious. We strongly recommend reading it alongside this article: The Power of Compounding and Long-Term Investing.

The shift from salaried to wealthy isn't just a habit change. It's a belief change: believing that the small, boring, automatic transfer you set up today will, over enough time, become a cascade that changes everything. The math guarantees it. But you have to stay in the game long enough for the math to do its work.

What to Do Starting This Month

You don't need a big salary review or a perfect financial plan to begin. Here are four concrete actions you can take before the month ends:

1. Calculate your emergency fund target. Add up your total monthly expenses (rent, EMIs, groceries, utilities, everything). Multiply by 3. That's your minimum emergency fund target. Check how far away you are.

2. Open a separate savings account or liquid fund. Your emergency fund should not live in your main salary account. Physical separation prevents accidental spending. A liquid mutual fund is ideal; it earns better than a savings account and can be redeemed in 1-2 business days.

3. Set up one SIP today, not next month. Even ₹2,000-₹5,000 in a simple large-cap or index fund is enough to start. The habit of investing matters more than the amount right now. You can increase it with every raise (ideally before you get used to the higher take-home).

4. Apply the 50/30/20 rule as a starting point. 50% of take-home toward needs, 30% toward wants, 20% toward savings and investments. If 20% feels too much, start with 10%. The exact number matters less than the fact that the investment goes out first, not last.

The key insight from the bucket framework is this: wealth is not what's left after you spend. Wealth is what you redirect before you spend.

Key Takeaways

| Concept | What It Means |

|---|---|

| Leaky bucket | Your salary drains through expenses and EMIs; income alone doesn't build wealth |

| The rich trap | Higher income just means a bigger hole; lifestyle inflation cancels out raises |

| Emergency fund | The first pipe that redirects savings before expenses, creating a safety net |

| Golden bucket | Money invested in equity mutual funds / SIPs that generates returns |

| The cascade | Returns from investments generating more returns; compounding at work |

| The shift | Wealth is built by habit, not salary; it starts with one automatic transfer |

Watch

Frequently Asked Questions

I earn ₹50,000 a month. Is it even worth starting to invest?

Yes, and urgently so. The earlier you start, the more time compounding has to work. Even ₹3,000–₹5,000 a month invested consistently in an equity mutual fund over 20 years can grow substantially. The amount you start with matters far less than that you start. Waiting until the salary is higher is the single most expensive financial mistake most salaried Indians make.

How is a SIP different from just saving money in a bank?

A Systematic Investment Plan (SIP) is a fixed amount invested automatically every month into a mutual fund, typically equity funds that invest in the stock market. Unlike a savings account that earns 3-4%, equity funds have historically delivered 10-14% annual returns over long periods (though past returns don't guarantee future performance). The key difference: savings preserve your money. SIPs have the potential to grow it significantly over time.

How much should my emergency fund be?

The standard recommendation is 3 to 6 months of your total monthly expenses. If your monthly expenses are ₹60,000, your emergency fund target is ₹1.8 to ₹3.6 lakh. If your job is less stable or you're self-employed, aim for the higher end. This should sit in a liquid mutual fund or high-yield savings account: accessible, but not so accessible that you spend it.

What if I have existing EMIs and loans? Should I invest or pay those off first?

It depends on the interest rate. High-interest debt (personal loans, credit cards at 18-36%) should generally be cleared first; those rates are higher than what equity investments can reliably earn. Low-interest debt (home loans at 8-9%) can coexist with investing. A simple rule: if the loan interest rate is above 10-12%, prioritise repayment. Below that, you can do both simultaneously.

I've been earning for 5 years and have almost nothing saved. Is it too late?

It is not too late. Wealth-building is not a race with a fixed start line; it's a process that begins whenever you begin. The most important thing is not how long you've been working; it's how long your money has to compound from today. A 32-year-old starting now still has 25+ years of runway before a typical retirement age. Start with Step 1 (emergency fund), move to Step 2 (a SIP), and stay consistent. The cascade will follow.

How do I choose which mutual fund to invest in?

For a first-time investor, a simple large-cap index fund (like a Nifty 50 index fund) is an excellent starting point. It's low-cost, diversified across India's 50 largest companies, and doesn't require you to pick stocks or time the market. As your investments grow and your financial knowledge deepens, you can diversify across fund categories aligned with your goals. If you're unsure, speaking with a SEBI-registered advisor or a mutual fund distributor who takes a goal-based approach is always a good idea.

Want to talk?

The path from salaried to wealthy isn't secret knowledge. It's the bucket framework: plug the leak, build the golden bucket, let the cascade begin. The only thing that makes it hard is starting. Everything after that is consistency.

Not sure which step you're on? Let's figure it out together: reach out to A2 Wealth and we'll help you map your buckets.

Related reading: The Power of Compounding and Long-Term Investing